Key Takeaways

- Insurance firms struggle with digital transformation due to competing priorities, which leads to delivery chaos and unfulfilled expectations.

- Traditional programme management fails to address the complexities of knowledge work, resulting in delays and increased frustration among stakeholders.

- Adopting Flow principles can optimise value delivery by limiting work in progress and visualising the entire value stream.

- Shifting to Product Operating Models enables teams to focus on continuous improvement and better manage transformation efforts over time.

- Implementing WIP limits and regularly reviewing Flow metrics are critical steps for building sustainable Insurance Digital Transformation Confidence.

Insurance firms are drowning in digital transformation initiatives whilst delivering little actual value. The problem isn’t technology capability or strategic vision – it’s the invisible chaos between them. When underwriting systems, claims platforms, and customer portals all compete for the same engineering capacity, delivery confidence collapses.

The hidden cost structure of Insurance transformation

Most insurance transformation programmes share a common failure pattern. Leadership commits capital to modernise legacy systems, improve customer experience, and unlock data analytics. IT roadmaps fill with worthy initiatives. Yet two years later, the organisation has partial implementations, frustrated stakeholders, and mounting technical debt, not to mention credibility debt incurred by those trying their best to implement.

The root cause is rarely execution capability. It’s systemic constraint blindness – the inability to see where work actually gets stuck, and what that delay is costing. In insurance, this manifests as competing priorities across underwriting, claims, compliance, and distribution channels. Each function believes its initiatives are urgent. Without transparent flow metrics, political capital determines sequencing rather than economic value.

Consider a mid-sized commercial lines insurer we observed. They had nineteen active technology initiatives, seven delivery teams, and no visibility into which projects were blocking others. Work sat waiting in queues for an average of forty-three days before anyone touched it. When leadership asked why transformation was taking so long, they received contradictory status reports and vague reassurances. The real answer was invisible: their delivery system had far too much work in progress relative to capacity.

Why traditional programme management fails Insurance transformation

Insurance organisations typically apply programme management disciplines developed for predictable, sequential work – great if you’re building a house, not so good for knowledge work. They create detailed Gantt charts, assign a RAG status to each line, and hold steering committees. These governance structures provide an illusion of control whilst the underlying delivery system remains chaotic.

The fundamental issue is that insurance transformation work is knowledge work, not construction. Unlike building a data centre or rolling out physical infrastructure, developing software and integrating systems requires experimentation, learning, and adaptation. Work doesn’t flow linearly from requirements through design to implementation. It iterates, blocks on dependencies, and reveals hidden complexity.

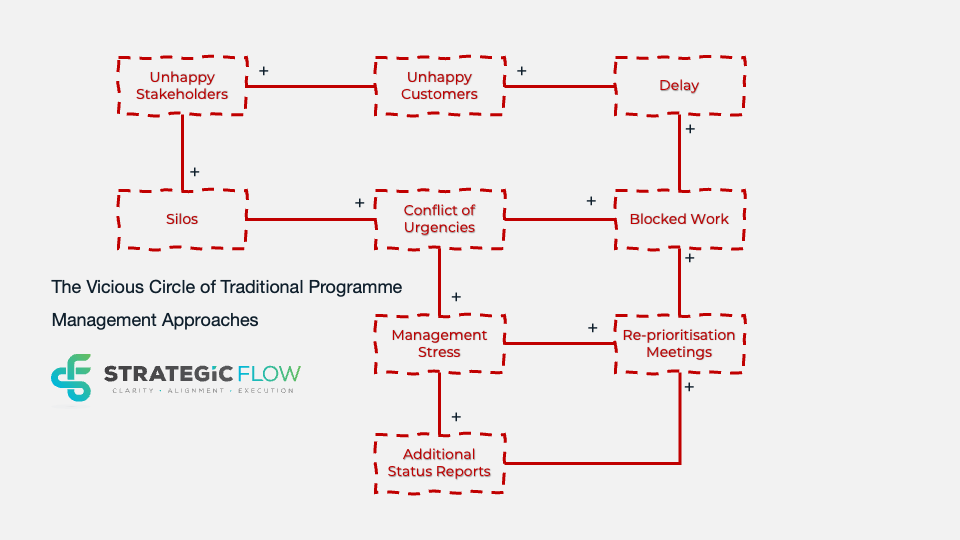

Traditional programme management responds to delays by adding more initiatives to the portfolio, hiring additional contractors, or demanding more detailed plans. Each response actually worsens flow. More concurrent initiatives increase context switching and coordination overhead. Additional people require onboarding and integration into existing team structures. More detailed planning creates false precision whilst delaying the learning that only comes from actually building and testing. The following illustration gives a partial glimpse into the problem:

This is a simplified Systems Picture of how knowledge work slows down and becomes difficult to get flowing. Teams tend to be structured into silos of specialism, each with it’s own set of priorities, which may, or may not, match the overall priorities of the organisation. These competing priorities conflict which creates management stress. This, in turn, causes management to panic so they seek additional status reports (that create additional work, thereby also reducing capacity) and multiple reprioritisation meetings (that take people away from doing work), all of which blocks work. Blocked work causes delays which, of course, creates unhappy customers who tend to complain to the relevant stakeholders who, in turn, complain to their contacts in the silos. And so it goes on, compounding and compounding.

The insurance sector faces particular challenges here. Regulatory compliance requirements create genuine constraints on what can be changed and when. Legacy system complexity means every change risks unexpected side effects. Customer-facing systems must maintain extremely high availability. These factors make rapid experimentation feel dangerous, yet they make flow optimisation even more critical.

Flow principles applied to Insurance systems delivery

Flow – the Lean principle of optimising for continuous delivery of value – offers insurance organisations a fundamentally different approach to transformation. Rather than managing projects and tracking completion percentages, Flow focuses on the movement of work through the delivery system and the constraints that impede it.

The Theory of Constraints provides the intellectual foundation. Every system has exactly one primary constraint that determines overall throughput. In insurance transformation contexts, this constraint is rarely individual team capacity. It’s usually architectural dependencies between systems, access to scarce specialist knowledge (sat outside the silos, or in alternate ones with their own priorities), or approval bottlenecks in governance processes.

Applying Flow principles means making three critical shifts. First, limit work in progress (WIP) to match actual capacity rather than aspirational roadmaps. Most insurance IT portfolios contain three to five times more active work than their delivery system can process efficiently. By capping the number of concurrent initiatives, organisations force explicit prioritisation decisions and dramatically reduce wait times.

Second, measure cycle time and throughput rather than resource utilisation and project completion. An initiative that takes nine months with three months of active work has six months of pure delay. That delay represents lost value-delayed premium growth, extended manual process costs, or prolonged customer friction. Cost of Delay (CD3) quantifies this economic impact and reveals which work genuinely cannot wait.

Third, visualise the entire value stream from strategic intent through to production deployment. Insurance organisations often have excellent visibility into individual team backlogs whilst having no idea where work is actually blocked. A Kanban board that spans from business case approval through architecture review, development, testing, compliance validation, and deployment makes constraints visible to everyone.

A European insurer applied these principles to their Personal Lines transformation. They reduced active initiatives from fourteen to five, implemented WIP limits at the portfolio level, and created a transparent flow board reviewed weekly by senior leadership. Within four months, their average delivery cycle time dropped from eleven months to six. More importantly, they could now predict completion dates (to around 83%) with genuine confidence rather than wishful thinking.

Product Operating Models vs project portfolios

The shift from project-based delivery to Product Operating Models represents perhaps the most significant structural change insurance organisations can make. Traditional project portfolios treat each initiative as a discrete effort with defined scope, timeline, and team. This creates constant organisational churn as teams form, deliver, and dissolve.

Product Operating Models instead organise around persistent value streams – stable, cross-functional, teams responsible for specific customer outcomes or business capabilities over time. Rather than assembling a project team to “implement a new claims system”, you establish a claims experience product team accountable for continuously improving how customers and colleagues interact with claims processes.

This structural shift has profound implications for delivery confidence. Persistent teams develop deep contextual knowledge about their domain, the systems they own, and the customers they serve. They make better architectural decisions because they’ll live with the consequences. They can balance short-term delivery pressure with long-term technical sustainability because they’re optimising for throughput over years, not just completing a project.

For insurance firms, Product Operating Models align naturally with functional domains: underwriting, claims, policy administration, customer portals, and data analytics each become product areas. Cross-functional teams combine business analysts, developers, designers, and operations engineers. They own outcomes (claims processing time, underwriting conversion rates, customer satisfaction) rather than outputs (features delivered, story points completed).

The transition isn’t trivial. It requires rethinking funding models, redefining leadership roles, and rebuilding planning processes. But the payoff is substantial: organisations can respond to market changes in weeks rather than navigating a nine-month project approval and delivery cycle. A UK motor insurer made this shift and reduced time-to-market for new coverage options from eighteen months to six weeks.

Kanban for strategic portfolio management

Whilst Kanban originated as a team-level workflow management practice, its principles scale powerfully to portfolio-level strategic decision-making. Strategic Kanban provides insurance leadership teams with real-time visibility into transformation capacity, initiative flow, and systemic constraints.

Kanban is actually way more than the boards people normally associate it with; however, the key is designing board structures that reflect how work actually moves through your organisation. For insurance transformation, this typically means columns representing strategic approval, architecture design, capacity allocation, active development, compliance review, and production deployment. Each column has explicit WIP limits based on actual processing capacity at that stage.

Tip: Don’t create a “Blocked” column for blocked work. Instead, block work items in situ in the flow. That way you get insights into blockage patterns which is much more meaningful.

This approach transforms portfolio governance from status reporting theatre into genuine strategic dialogue. Leadership discussions focus on: Where is work blocked? What constraint do we need to address? Which initiatives should we start next given current capacity? These questions drive meaningful decisions rather than reviewing predetermined status updates.

Initiatives flow across the board as they complete each stage. Leadership doesn’t track percentage complete or RAG status, they track movement. An initiative stuck in architecture design for eight weeks reveals a constraint that needs attention (if you move it to a blocked column, you lose the insight that architecture design may have a constraint that needs addressing). Three initiatives waiting for compliance review signals either insufficient review capacity or unclear requirements being submitted (ditto).

Data management initiatives – critical for modern insurance transformation – particularly benefit from this transparency. Integrating data across legacy policy administration, claims systems, and new digital platforms involves complex dependencies across multiple teams and technologies. Without flow visibility, these initiatives drag on for years. With explicit WIP limits and transparent board states, leadership can see exactly where data integration is blocked and take targeted action.

Practical next steps for Insurance leaders

If you recognise these patterns in your organisation, three actions will begin building delivery confidence:

First, map your current flow. Identify every active transformation initiative and plot where it sits in your delivery process – approved but not started, in design, actively being built, waiting for testing, pending deployment (tailor to your context). Count the work at each stage and compare it to your actual processing capacity. This diagnostic typically reveals enormous hidden queues and surprising constraints.

Second, implement portfolio WIP limits. Cap the number of initiatives in active development to match your delivery capacity, likely 40-60% of your current active count. Force explicit prioritisation using economic criteria – Cost of Delay, classes of service (a useful proxy for Cost of Delay if you want to get started quickly), strategic value, or risk reduction. Accept that this means pausing or cancelling some work. The alternative is everything taking longer whilst nothing delivers value.

Third, establish a regular cadence for reviewing Flow metrics. Weekly or fortnightly, examine cycle times, throughput rates, and where work is blocked. Make these sessions about systemic problem-solving, not status reporting or finger pointing. When an initiative is delayed, ask what constraint caused the delay and what systemic change would prevent recurrence.

These changes don’t require wholesale organisational redesign or new technology platforms. They require leadership commitment to making work visible, limiting overload, and optimising for flow rather than resource utilisation.

Building sustainable transformation capability

Insurance digital transformation fails when organisations treat it as a series of projects to complete. It succeeds when they recognise it as building permanent capability to deliver strategic change reliably and rapidly. That capability emerges from systemic design: transparent flow, constrained work in progress, product-oriented team structures, and economic prioritisation.

The organisations achieving genuine delivery confidence aren’t necessarily more technically advanced or better funded. They’ve made their delivery systems visible, identified and addressed systemic constraints, and organised around value flow. They can commit to business outcomes with genuine confidence because they understand their throughput capacity and protect it rigorously.

The insurance sector faces extraordinary transformation pressure – customer expectations shaped by digital natives, regulatory evolution, climate risk complexity, and operational cost challenges. Firms that build sustainable delivery capability will shape their markets. Those that remain trapped in project chaos will struggle to keep pace.

Strategic Flow would welcome a conversation if you’re exploring how Flow principles, Kanban, and Product Operating Models can transform your insurance transformation from initiative chaos into confident value delivery.